Buying a home is one of the biggest financial milestones in a person’s life. It’s an emotional decision, but it’s also a massive financial commitment, usually funded by a home loan that runs for 20-30 years. To make homeownership more accessible and to encourage investment in real estate, the Indian government provides significant tax benefits on home loans.

These tax breaks are a powerful tool for reducing your overall tax liability, but they are spread across two different sections of the Income Tax Act. This often leads to confusion. Many homeowners aren’t aware of the total benefits they can claim or the specific conditions attached to each, potentially leaving thousands of rupees in tax savings on the table each year.

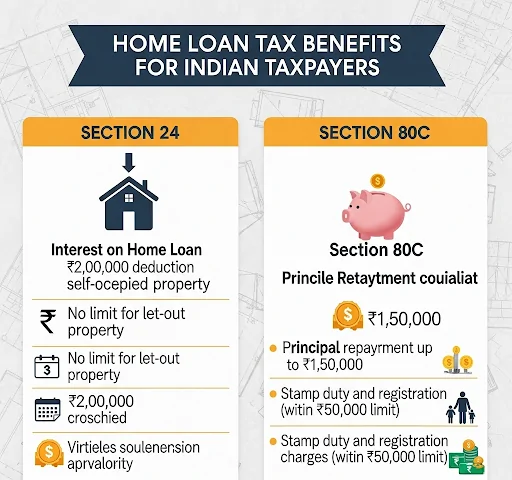

This guide will demystify the entire process. We will break down the two main pillars of home loan tax benefits—**Section 24(b)** for interest repayment and **Section 80C** for principal repayment—and explain exactly how you can claim them to maximize your savings.

The Two Pillars of Home Loan Tax Savings

Every EMI (Equated Monthly Installment) you pay for your home loan consists of two parts: the **principal amount** and the **interest amount**. The good news is that you can claim tax deductions on both components, but under different sections with different limits.

- Deduction on Interest Paid: Claimed under **Section 24(b)** of the Income Tax Act.

- Deduction on Principal Repayment: Claimed under the well-known **Section 80C**.

Understanding both is key to making the most of your home loan. You can see the breakdown of your principal and interest payments by using a Home Loan EMI Calculator, which provides a detailed amortization schedule.

Pillar 1: Tax Benefit on Interest Paid under Section 24(b)

This is often the most significant tax benefit, especially in the early years of a home loan when the interest component of your EMI is very high. Section 24(b) allows you to claim a deduction on the interest you pay on your home loan from your “Income from House Property”.

For a Self-Occupied Property

A self-occupied property is one where you or your family members live.

- You can claim a maximum deduction of **₹2,00,000** per financial year on the interest paid.

- This deduction can be claimed from the financial year in which the construction of the house is completed and you have taken possession.

For a Rented-Out Property

If you have bought a house and rented it out, the rules are more generous.

- There is **no upper limit** on the interest you can claim as a deduction. The entire interest amount paid during the year can be claimed against the rental income.

- If the interest paid is more than the rental income, it creates a “loss from house property”. This loss can be set off against other income (like salary) up to a cap of **₹2,00,000** per year. Any remaining loss can be carried forward for up to 8 subsequent assessment years.

Conditions to Claim the Full ₹2 Lakh Deduction

To claim the maximum ₹2,00,000 deduction on a self-occupied property, you must meet these conditions:

- The loan must be taken on or after April 1, 1999, for the purchase or construction of a new property.

- The purchase or construction must be completed within **5 years** from the end of the financial year in which the loan was taken.

- If these conditions are not met, the interest deduction limit drops to just ₹30,000.

What About Pre-Construction Interest?

This is a very common scenario. What if you start paying EMIs while the property is still under construction? The interest you pay during this period is called pre-construction interest. You cannot claim it while the construction is ongoing. However, you don’t lose the benefit.

The total pre-construction interest can be claimed as a deduction in **five equal installments**, starting from the year in which the property construction is completed and you take possession. This deduction is part of the overall ₹2,00,000 limit for a self-occupied property.

Pillar 2: Tax Benefit on Principal Repayment under Section 80C

This is the second part of the tax benefit. The principal portion of your home loan EMI is eligible for a deduction under Section 80C of the Income Tax Act.

This is the same Section 80C that forms the backbone of tax-saving for most individuals and covers investments like ELSS, PPF, and NSC.

- The maximum deduction you can claim for principal repayment is **₹1,50,000** per financial year.

- This ₹1,50,000 limit is the **overall limit for Section 80C**. This means your home loan principal repayment, along with your other 80C investments (like PPF, ELSS, insurance premiums, etc.), cannot exceed ₹1.5 Lakhs in total.

- You can also include charges like stamp duty and registration fees paid during the purchase of the house under this section, but only for the year in which these expenses were incurred.

Important Lock-in Period for Section 80C

There’s a crucial condition attached to this benefit. You must not sell the property within **5 years** from the end of the financial year in which you took possession. If you sell the house before this 5-year period, the tax deductions you claimed on the principal repayment in the previous years will be reversed and added back to your taxable income in the year of sale.

Maximizing Benefits with a Joint Home Loan

Taking a joint home loan with a co-borrower (who must also be a co-owner) is a popular and powerful tax-saving strategy. If both co-borrowers are also co-owners and are paying the EMIs, then **each individual can claim these tax benefits separately**.

- Each co-borrower can claim a deduction of up to **₹2,00,000** on interest under Section 24(b).

- Each co-borrower can claim a deduction of up to **₹1,50,000** on principal under Section 80C (within their respective 80C limits).

This effectively doubles the potential tax benefit for the family, making it a highly efficient way to manage a large home loan.

Practical Steps: How to Claim Your Home Loan Tax Benefits

Understanding the rules is one thing; claiming the benefits is another. Here’s a simple step-by-step process:

- Get Your Home Loan Interest Certificate: At the end of each financial year, your bank or lending institution will provide you with a home loan statement or certificate. This crucial document gives a detailed breakup of how much principal and interest you have paid during that year.

- Submit to Your Employer: You can submit this certificate to your employer as part of your annual investment proof submission process (usually done between January and March). Your employer will then factor in these deductions while calculating your TDS (Tax Deducted at Source) for the remaining months.

- Claim in Your ITR: Whether you’ve submitted the proof to your employer or not, you must declare these deductions when filing your Income Tax Return (ITR). You will need to fill in the details of the interest paid (under ‘Income from House Property’) and the principal repaid (under Chapter VI-A deductions for Section 80C).

Summary of Home Loan Tax Benefits

| Benefit Component | Applicable Section | Maximum Deduction (Self-Occupied) | Key Conditions |

|---|---|---|---|

| Interest on Loan | Section 24(b) | ₹2,00,000 per year | Construction must be completed within 5 years. Claimable after possession. |

| Principal Repayment | Section 80C | ₹1,50,000 per year (within the overall 80C limit) | Property cannot be sold within 5 years of possession. |

The Final Word: A Powerful Wealth-Building Tool

The tax benefits on a home loan are substantial and can save you lakhs of rupees over the loan tenure. By combining the deductions under Section 24(b) and Section 80C, a homeowner can claim a total deduction of up to **₹3,50,000** (₹2,00,000 for interest + ₹1,50,000 for principal) in a single year. If it’s a joint loan, this benefit can be even higher.

This makes buying a home not just a step towards stability but also a very effective tax-planning strategy. Make sure you get your home loan interest certificate from your bank every year and use it to claim these benefits when filing your tax returns, turning one of your biggest expenses into one of your biggest savings.